For today’s digital economy, payments are not a simple pipeline from customer to merchant. They’re an ecosystem of providers, rails, risk engines, and regional methods. For high-risk merchants — subscription models, creator platforms, global ecommerce — this complexity isn’t theoretical. It directly impacts revenue, conversion, and cash flow.

This article explains why payment orchestration matters, and backs it up with real data, reports, and examples from trusted industry sources.

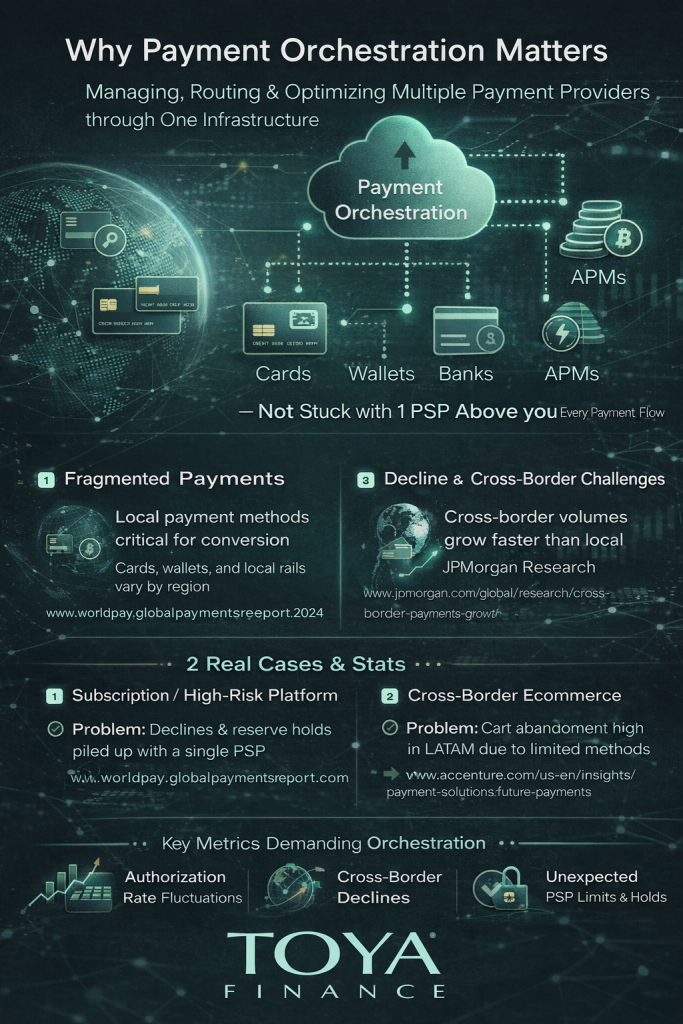

What Is Payment Orchestration?

Payment orchestration centralizes payment logic across multiple providers and methods. Instead of relying on a single PSP, merchants route transactions through a managed layer that intelligently selects:

- the best provider per transaction

- fallback routes for declines

- cost-optimized payment rails

- unified reconciliation and reporting

Without orchestration, merchants often encounter:

- inconsistent routing decisions

- fragmented reporting

- manual reconciliation

- lack of decline handling strategies

This limitation is well documented by industry research.

The Case for Orchestration — What Data Shows

1) Fragmentation of Global Payments

According to the Worldpay Global Payments Report 2024, payment preferences vary significantly by region. While cards dominate in North America and Europe, local digital wallets and bank redirects lead in Asia and LATAM.

“Local payment methods are critical to conversion in many markets, and a single-rail approach limits global reach.”

— Worldpay Global Payments Report 2024

🔗 https://worldpay.globalpaymentsreport.com/

This divergence implies that multiple rails must be managed centrally — not bolted on.

2) Declines & Cross-Border Challenges

A research note from JPMorgan’s Global Data highlights that cross-border payment volumes are growing faster than domestic ones, leading to greater reliance on multiple rails and partners to manage declines and settlement times.

🔗 https://www.jpmorgan.com/global/research/cross-border-payments-growth-2025

Key takeaway:

- cross-border complexity increases declines

- multi-rail strategies reduce friction

- orchestration enables dynamic choice of providers

3) Authorization & Routing Optimization

According to an Accenture Payments Report, merchants that implement analytics-driven routing see material improvements in authorization rates.

Merchants using automated routing and analytics can see up to 10-15% higher authorization rates compared to static routing.

— Accenture “Future of Payments” Report

🔗 https://www.accenture.com/us-en/insights/payment-solutions/future-payments

This highlights the value of data-driven orchestration rather than adding more PSPs manually.

Real Scenarios Where Orchestration Matters

Example 1 — Subscription / High-Risk Platform

Problem: A subscription platform lost revenue due to frequent declines and rolling reserves imposed by single PSP.

Orchestration Approach:

- Multiple PSP integrations

- Routing by geo performance

- Automated fallback paths

- Central visibility into declines

Result:

Authority declines fell, revenue leakage reduced, and cash flow became more predictable.

This problem and solution pattern aligns with real merchant cases documented by fintech publications:

🔗 “Subscription merchants are increasingly using smart routing to avoid single-provider risk,” — Finextra Insight

https://www.finextra.com/blogposting/25476/surviving-high-risk-payments-with-smart-routing

Example 2 — Cross-Border Ecommerce

Problem: An ecommerce brand saw higher abandonment rates in LATAM due to limited acceptance and high card fees.

Orchestration Approach:

- Real-time routing across PSPs

- Local wallets + bank redirects

- Fallback to alternative rails

Result:

Improved checkout completion and reduced cost per transaction.

This trend is echoed in this analysis:

🔗 “Cross-border ecommerce growth drives multi-rail payments adoption” — PaymentsJournal

https://www.paymentsjournal.com/cross-border-ecommerce-multi-rail-adoption/

Orchestration vs. Traditional Aggregators

Traditional PSP aggregators combine payment methods but often do not provide:

✔ vendor independence

✔ dynamic routing

✔ decline fallback logic

✔ central risk strategy

✔ unified analytics

Payment Orchestration Platforms do provide these, and this difference has been highlighted by Forrester and Gartner, noting the emergence of orchestration as a strategic layer:

🔗 Forrester: “The Rise of Payment Orchestration Platforms”

https://www.forrester.com/report/the-rise-of-payment-orchestration/

(subscription may be required)

Analytics & Risk Controls Are Core

Orchestration without analytics is blind.

Critical analytics features include:

- decline reason tracking

- cost vs. acceptance benchmarking

- currency and settlement performance

- provider thresholds and risk triggers

A McKinsey Report on Digital Payments emphasizes:

“Improving authorization, routing efficiency, and cross-rail performance requires strong data and real-time insights.”

🔗 https://www.mckinsey.com/industries/financial-services/our-insights/next-gen-payments

Key Takeaways

High-risk digital businesses must build payment stacks that:

- Diversify payment methods — cards, wallets, local rails, crypto

- Centralize orchestration logic — one layer controlling all rails

- Use data to drive routing & decline recovery

- Mitigate risk holistically — not per PSP

Payments are no longer a commodity. They are infrastructure — and orchestrated infrastructure delivers resilience, conversion, and revenue predictability.